At the end of each fiscal year, quickbooks will close out your yearly income and expense accounts automatically. However, users still have the ability to go back to a previous date and add a transaction or change a transaction. It is also common for a user to unintentionally change an entry from a prior period. It happens way too often.

Probably around 60% of the clients I have dealt with have made various changes in prior periods. Unless assisted by a CPA, this is never a good thing to do, no matter how great of an idea it seems to be at the time. Many users will decide to make these changes after they discover an error in a prior period. They believe a quick change will fix everything.

The problem is that reconciled books have to be consistent from one period to the next. If there is a change made after the monthly reconciliation, or a change made after journal entries were made by the accountant, then the user’s adjustment could have some unintended consequences. This is even more of a problem when the changes were for a prior year and your company’s federal income taxes for the have been filed. It will suddenly become much harder to reconcile your books to your tax return. You will have to dig through many new transactions in the prior year to account for all the changes that were made after the taxes were prepared. And if the IRS comes knocking, it will be much harder to explain how you manufactured your taxable income from your book income.

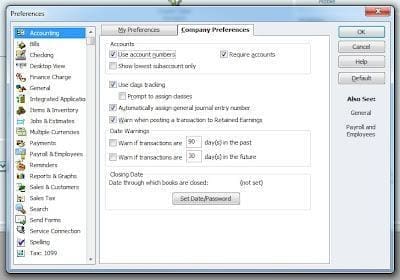

Thankfully, quickbooks does give you the option to ensure that the prior period is safe from updates. Once you have opened your company file in quickbooks, go to Edit/Preferences. Find the Accounting Preference in the left pane, then click the company preferences tab.

Now click the Set Date/Password button at the bottom. At this point, you should be here:

In the closing date field, enter the date after which you don’t want any changes made. This is usually going to be December 31 of the previous year. This should keep you safe from future changes that could have damaging effects on your financial statements.

Feel free to contact Evan Hutcheson, CPA with any questions. I have had the luxury of working with some very messy books from many unique clientele over the years.

Divya Mehta

How we can add transactions as Prior period adjustments? What should be the account and detail type of Prior Period adjustments?